Trends Analysis - Q4 2022

February 12, 2023

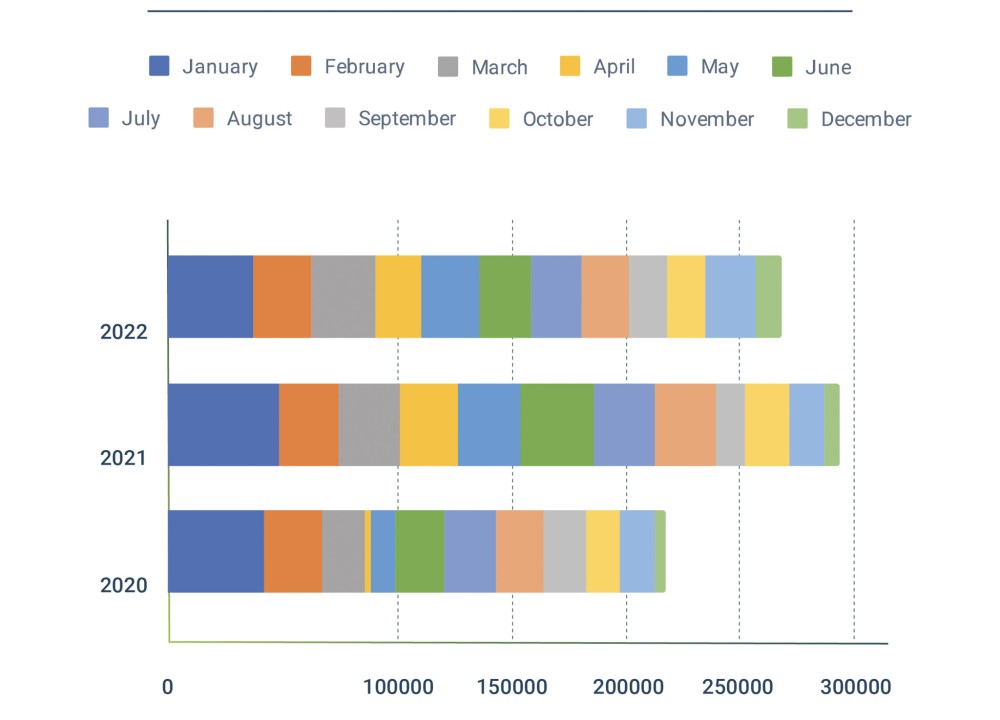

Registration Data

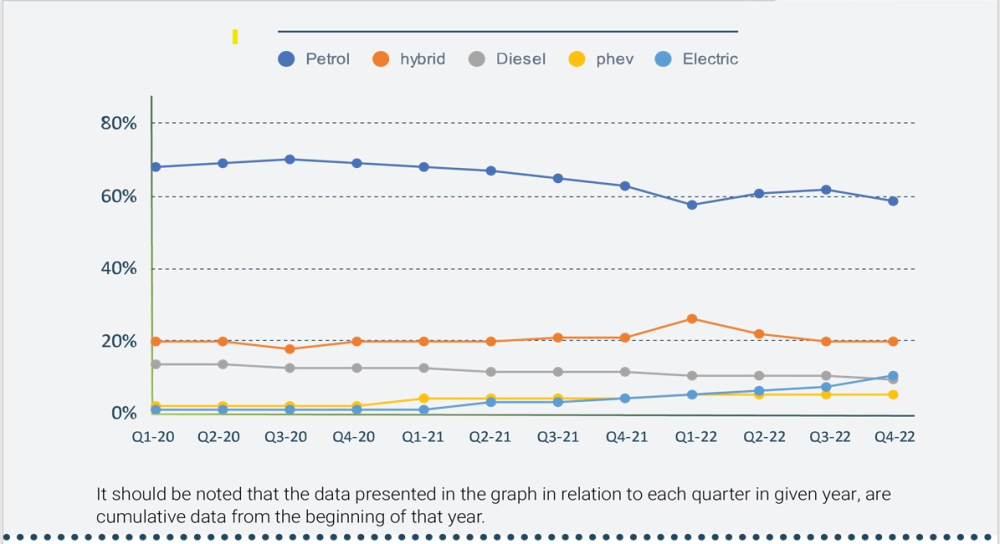

Registration by Engine Type

After the increase in demand observed in the previous two quarters, the demand for petrol cars in the last quarter of 2022 makes up 56% of all new vehicles, which is almost the same demand observed in the year's first quarter. In Q4 2022, petrol's share of the Israeli car market declined by 3% compared to Q3 2022. Compared to the same period last year, the demand for petrol vehicles in Q4 2022 decreased by 4%, and in the same period in 2020 decreased by 10%.

The demand for Hybrid Electric Vehicles in Q4 2022 remained unchanged compared to Q3 2022 and makes up 19% of all new vehicles, almost the same demand which was observed in Q4 2021 and Q4 2020. Hybrid Electric Vehicles are the most significant volume category of Alternatively Powered Vehicles in Israel.

The demand for electric vehicles in Israel continues its upward trend and increased by 3% compared to Q3 2022 and by 6% compared to Q4 2021, and 9% compared to Q4 2020.

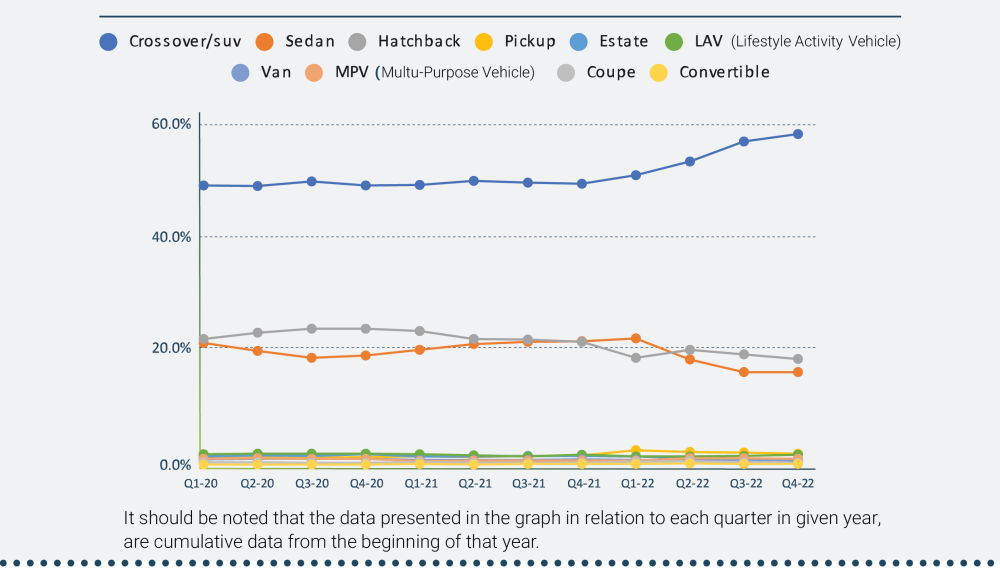

Registration by Segment Type

The demand for Crossover/SUV has remained stable over the past years and continues to lead the market; when in Q4 2022, another increase was observed when Crossover/SUVs hold 58% of all new vehicles, a rise of 1.3% compared to Q3 2022 and of 8.7% compared to Q4 2021 and of 9% compared to Q4 2020.

Sedan and Hatchback have been the second volume category of new vehicles in Israel in the past years. In Q4 2022, a slight decrease of 0.8% was observed in demand for Hatchback vehicles compared to Q3 2022, and it makes up 18.6% of all new vehicles, a reduction of 3% compared to Q4 2021 and 5.3% compared to Q4 2020.

The demand for Sedan vehicles remained the same compared to Q3 2022 and makes up 16.3% of all new vehicles, a decrease of 5.4% compared to Q4 2021 and 2.9% compared to Q4 2020.

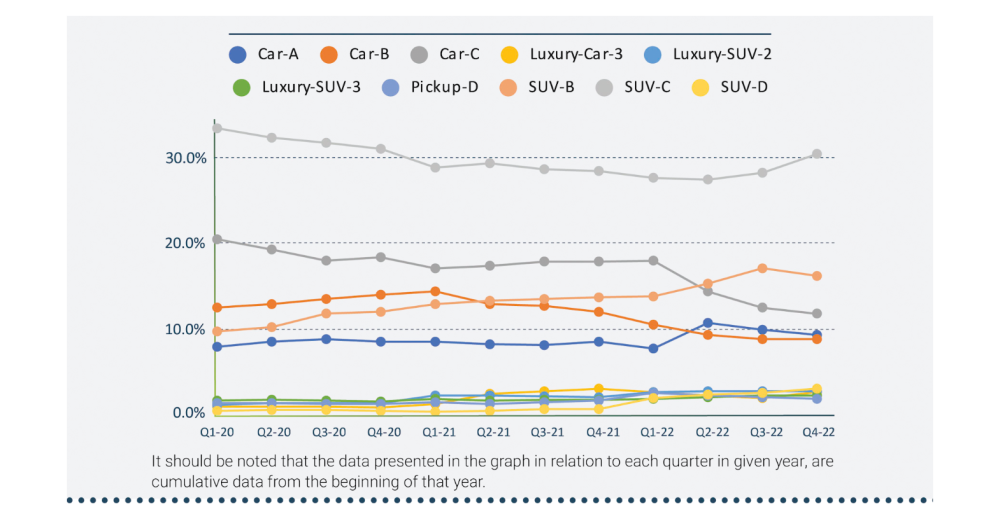

Registration by Category

The SUV-C category leads the market of new vehicles, when from July to Sep 2022, there was indeed an increase of 0.8% compared to Q2 2022, however, such category slightly reduced to 28.4%, compared to 28.8% in the corresponding period in 2021 and significantly reduced compared to 31.9% in the corresponding period in 2020. The demand for the Car-C category in Q3 2022 continued its downward trend and declined by 1.9% compared to Q2 2022 and make up 12.6% of all new vehicles, compared to 18% in the corresponding period in 2021 and 18.1% in the corresponding period in 2020. In contrast, the demand for Suv-B continued its upward trend also in Q3 2022 with 17.2%, an increase of 1.8% compared to Q2 2022, which makes it the second volume category of new vehicles in Israel. The demand for such category rose by 3.6% compared to July-Sep 2021 and 5.3% compared to July-Sep 2021. The demand for Car-B category, is on a downward trend (after an increase in demand was observed during 2020) with 8.9%, an increase of 3.9% compared to July-Sep 2021 and of 4.7% compared to July-Sep 2020. The demand for Car-A category registered a decrease of 0.8% in Q3 2022 compared to Q2 2022, and makes up 10% of all new vehicles.

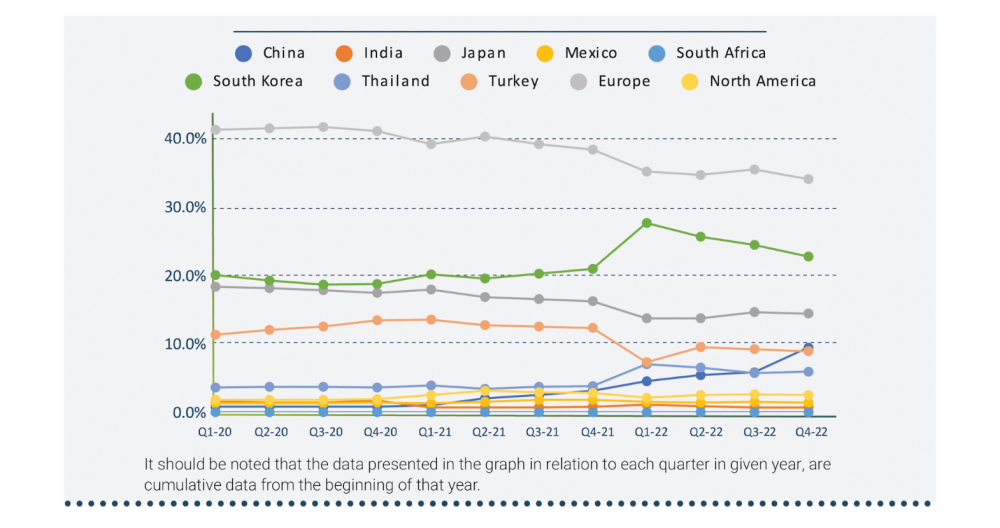

Registration by Country of Origin

As of Q4 2022, 34% of all new vehicles are manufactured in Europe, a decrease of 4.3% compared to Q4 2021 and 7% compared to Q4 2020.

After an increase in demand for vehicles manufactured in South Korea in Q1 2022 and Q4 2022, another decrease of 1.7% was observed compared to Q3 2022, and such vehicles make up 22.7% of all new vehicles. However, it's still an increase of 1.8% compared to Q4 2021 and 4% compared to Q4 2020. The demand for vehicles manufactured in Japan in Q4 2022 remained almost unchanged and makes up 14.4% of all new vehicles. The demand for Vehicles manufactured in Turkey also remained practically unchanged; in Q4 2022, such vehicles make up 8.9%. It should be noted that the demand for new vehicles from these two countries is downward compared to previous years. On the other hand, it can be observed that there is an upward trend in demand for vehicles manufactured in China, which in Q4 2022 makes up 9.4% of all new vehicles, an increase of 6.3% compared to Q4 2021 and 8.6% compared to Q4 2020.