Trends Analysis of the Israeli market for new vehicles - Q1 2023

May 10, 2023

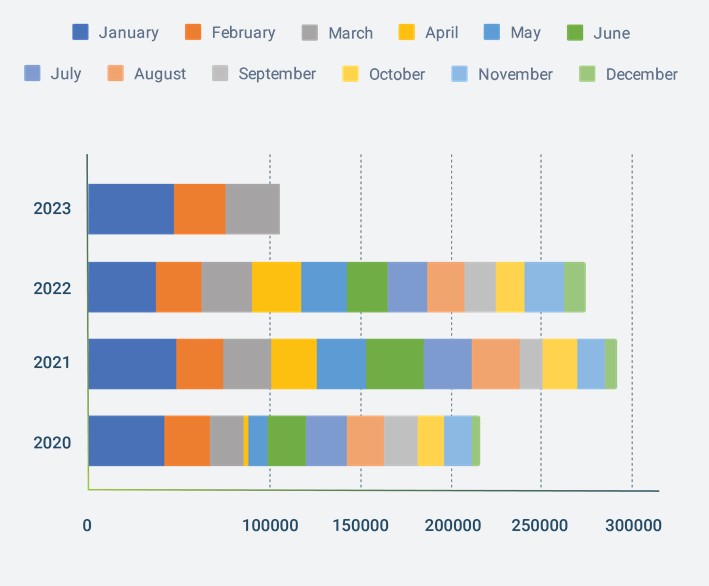

Registration Data

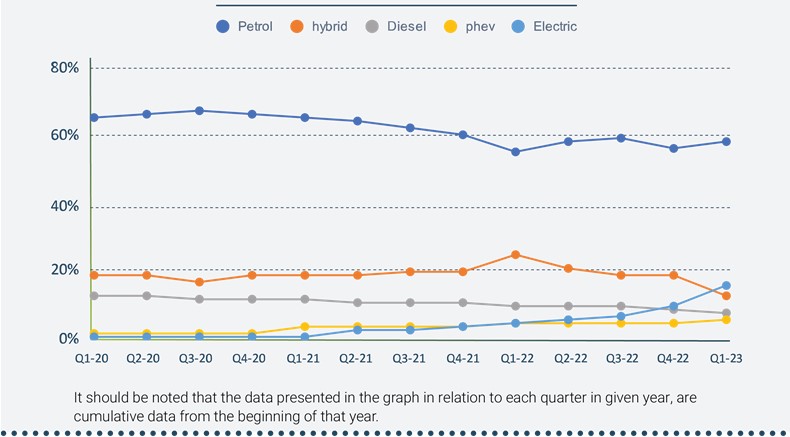

Registration by Engine Type

In the first quarter of 2023, the demand for petrol cars in Israel increased and made up 58% of all new vehicles, following a decrease in demand in the last quarter of 2022. Petrol's share of the Israeli car market grew by 2% compared to Q4 2022. In comparison to the same period in 2022, the demand for petrol vehicles in Q1 2023 increased by 3%, while it decreased by 7% compared to the same period in 2021.

On the other hand, the demand for electric vehicles continued to show an upward trend, increasing by 6% compared to Q4 2022, 11% compared to Q1 2022, and 15% compared to Q4 2020. In Q1 2023, electric vehicles made up 16% of all new vehicles, solidifying their position as the most significant volume category of Alternatively Powered Vehicles in Israel.

However, the demand for Hybrid Electric Vehicles continued its downward trend, making up only 13% of all new vehicles in Q1 2023. This marks a decline of 6% compared to Q4 2022 and 12% compared to the same period a year ago.

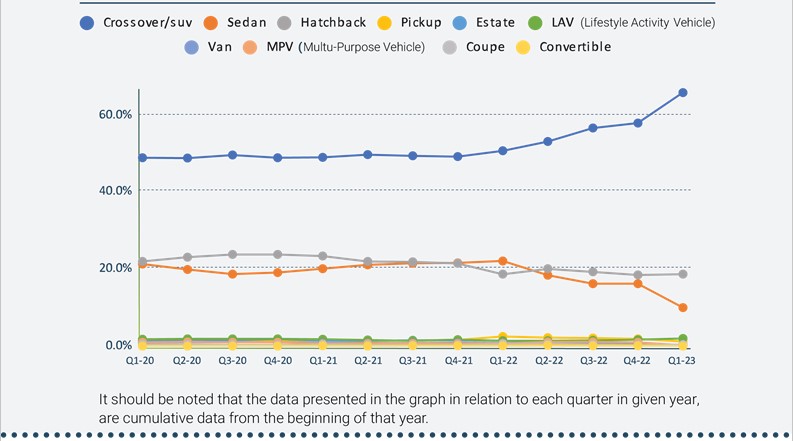

Registration by Segment Type

The Crossover/SUV segment of the Israeli new vehicle market has maintained stability in demand over the past few years, with a continuous lead in the market. In Q1 2023, this segment experienced a significant increase, holding 65.9% of all new vehicles, which is an increase of almost 8% compared to Q4 2022 and 15% compared to Q1 2022. In comparison to Q1 2021, the increase is nearly 17%.

The Hatchback vehicle segment has remained stable throughout the years and makes up 18.8% of all new vehicles in Q1 2023, placing it as the second volume category of new vehicles in Israel.

The demand for Sedan vehicles is on a downward trend, comprising 10.1% of all new vehicles in Q1 2023, which is a decrease of 12.1% compared to Q1 2022 and 10.1% compared to Q1 2021.

Registration by Category

In Q1 2023, the SUV-C category continues to lead the market of new vehicles in Israel, with an additional increase of 5.3% compared to Q4 2022, making up 35.9% of all new vehicles. This is an 8.1% rise compared to the corresponding period in 2022 but a 6.9% decrease compared to the corresponding period in 2021.

The SUV-B category saw an increase in demand, making up 16.9% of all new vehicles, compared to 13.9% in the corresponding period in 2022 and 13% in the corresponding period in 2021, placing it as the second volume category of new vehicles in Israel.

However, the Car-C category continues its downward trend and only makes up 7% of all new vehicles in Q1 2023, reflecting a decrease of nearly 5% compared to Q4 2022, 11.1% compared to Q1 2022, and 10.2% compared to Q1 2021.

Registration by Country of Origin

In Q1 2023, European manufactured vehicles accounted for 31.9% of all new vehicles registered in Israel, which indicates a 3.2% decline compared to the same period in the previous year and a 7.2% decrease compared to Q1 2021.

In contrast, the demand for vehicles produced in South Korea showed a downward trend, making up 18.5% of all new vehicles in Q1 2023, which is a decline of 9.1% compared to Q1 2022 and 1.6% compared to the corresponding period in 2021.

Conversely, there has been a noticeable increase in the demand for vehicles manufactured in China, accounting for 17% of all new vehicles in Q1 2023, reflecting a surge of 12.5% compared to Q1 2022 and 16% compared to Q1 2021.

The demand for vehicles produced in Japan and Turkey remained relatively stable, with a percentage share of 13.5% and 9.1% of all new vehicles sold in Q1 2023, respectively.